Lots of people have an outdated opinion of manufactured homes. Whenever they hear the word mobile or manufactured they conjure up images of small, thin-walled campers that can be pulled behind a vehicle.

Does the manufactured home above look like it can be pulled behind anything?

The Palm Harbor manufactured home model you see above (and below) is indicative of a modern manufactured home. This is a premium model that is absolutely comparable to a site-built home in every way. It looks like a traditional home and it acts like a traditional home – its energy efficient, has the same framing, uses the same construction materials, and can be customized (and that’s just four things, there are several more). The only difference is that the manufactured home takes advantage of a technologically advanced factory setting and is built on a chassis.

Related: How Manufactured Homes are Constructed

Budget, Mid-Range, and Premium Homes

Even the mid-range and low-range manufactured homes have lots in common with site-built homes. Regardless of the price per square foot and the amenities offered, every manufactured home uses the same materials that a site-built home uses.

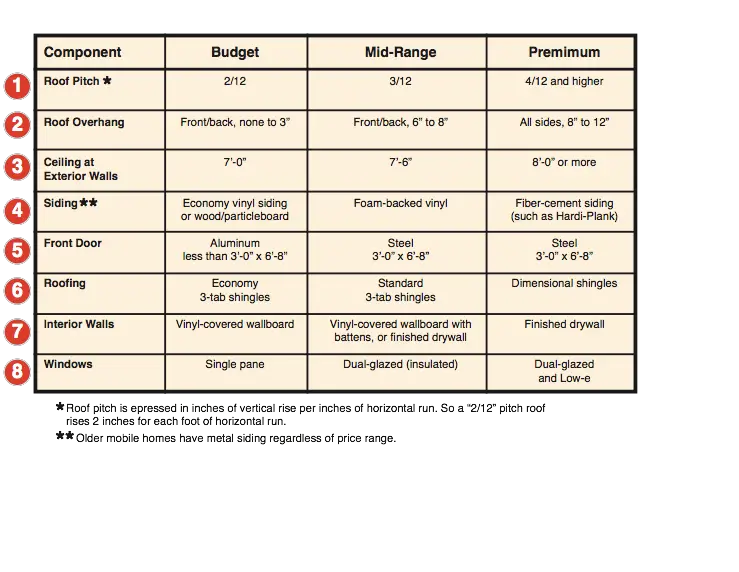

There are three price points for both site-built and manufactured home. Not all homes have marble countertops! The most affordable manufactured homes are the budget homes. Those are the homes you’ll see most often on dealer’s lots. They are great homes at great prices! They simply use more affordable materials and are usually smaller. Oftentimes, they will use thinner framing and lower pitched roofing. This does not mean the home is inferior, it is simply built for those that have a smaller budget.

The mid-range manufactured home is similar to a site-built home in just about every way. They have similar framing, roof pitch, material, and amenities. Yet, they are more affordable than a site-built home because being built in a factory allows the builder to control aspects that cannot be controlled with a site-built home. Builders are able to buy material in bulk, reduce construction time, and control material waste better. Having more control over the building process offers significant savings.

The premium manufactured home is comparable to custom site-built homes with high-end materials. These factory-built homes can still be offered at a lower price-per-square foot over the site-built home. Here’s a chart I found on a very informative inspection site called McGarry and Madsen (they have lots of great information about buying manufactured homes) that explains the three price ranges often offered in the manufactured home industry:

6 Things Manufactured Homes and Site-Built Homes have in Common

Here’s a graphic that shares what manufactured homes and site-built homes have in common. It’s a perfect resource for anyone that has an outdated opinion.

Don’t let the term manufactured fool you! These are great homes that are affordable. There’s a manufactured home for every budget and every need.

Thanks so much for reading Mobile and Manufactured Home Living!

Hi Brittany,

This stuff is crazy complicated! I just went through 3 years of saving and working on my credit so I could buy a new home. I wanted a double wide with a high pitched roof permanently installed on a small lot in SC. I did not want to go through ‘dealer financing.’ No bank would touch me because I didn’t have a 20% down payment. The FHA loans that are available for those without a huge down payment won’t cover manufactured homes or condos so I was stuck. I did check on financing through a company (I’ll not mention names) but their interest rate was crazy. They said it was because my credit score was too low – home financing does not use the credit score that you see on all those credit apps and credit card accounts. There are around 8 different formulas they use to calculate a credit score and home buying has one of the most stringent formulas. For example, a buyer shows a credit score of 730 on Credit Sesame (or whatever credit score app or credit card account that show you a free credit score each month) but using the home financing formula shows a credit score of 648. I was told it is a formula that basically tells the financiers how likely you are to miss a payment within 24 months of the loan.

I didn’t get that double wide with the high roof but had I tried a little harder with the dealerships I would have been able to get a loan, I’m sure. It would have been a little higher interest than I wanted though.

I’m not sure what Clayton’s rules are on their financing but I’m sure they will do whatever they can to help. If I can just recommend one thing: don’t buy the property and the home together if you don’t have to. Buy the property first and pay on it for a year and then buy the home. This may allow you to use the property as collateral and lower your rates and it may also keep you from paying a lot more for the land (interest wise) than it would be worth. Also, if anything should happen and you can’t pay for the home you can keep the land and move in a cheap mobile home. I am not knowledgeable about the dealer packages where they sell the land and home in a cute community (though I’ve driven through them and they are super nice!) so I can’t help there.

Credit is such an over-complicated mess. It’s unfair to a fault and the whole scoring system needs an overhaul.

Let me know how it goes and what you learn as you research if you can. Best of luck!

We’re looking to buy a manufactured home and some land to put it on. We will be first time home buyers. I’m unsure of how this all works. We’re trying to build our credit, save money and hopefully plan to buy in the next two years.we are going to avoid dealer fiancing but if we go through our bank would Clayton homes still help with finding the land?

Hi Kathy!

I have a few opinions regarding the problems manufactured homeowners face but I think when it’s all said and done it’s the stigma and misinformation surrounding our homes that hurts the most. This is especially true in regards to laws, financing, etc.

Banks don’t want to finance because the historical data shows the homes as being bad investments. Of course, they never differentiated from the types of manufactured homes (there are 3 ‘levels’ of manufactured homes – the lowest level is the cheapest models available, the middle level is the models that more resemble the construction of a site-built home, and the top level are the high end luxury homes that cost as much, if not more than a site-built home).

Combined together, manufactured homes typically do not increase in value if there is no land included (like a site-built home can) and because they are more affordable the average buyers are typically lower income earners and have more credit issues so banks can’t make the profit they can with site-built homes (there’s also the ‘idea’ that our homes can be moved easily which is completely untrue).

HUD is in charge of our national construction and installation regulations and they have been slow to update and enforce rules that could have made the homes a lot safer or last a lot longer (proper installation). There’s also finance laws that have been passed that supposedly protects homeowners from bad finance deals but seem to put a huge hindrance on manufactured home buyers due to their lower average credit scores and higher interest offers. There’s local laws that ban single wide within town limits, etc. Basically, we have tons of fights to fight!

I love your passion and desire to want to make changes! There are so many areas that need changes to help keep affordable housing available. HUD, FHA, and your local and state laws are a good place to start.

Thanks so much!

Crystal,

I have been trying to find out who makes the rules about mobile/manufactured homes. I love my 2100+ sq. ft home. What makes me mad is that the financial people consider it inferior. Financing and insuring is limited. When I get calls for “government programs” for energy, etc. my home does not qualify. I want to know why. I want to know who makes those rules. Do you have any idea. I am ready to challenge those rules. Just need to know where to start.

I really enjoy MHL magazine. Since I discovered it a few months ago, I look forward to each new issue—and, I read past issues over and over. Living in our manufactured home is wonderful! I have capitalized on many of the great decorating ideas shared in MHL. Thanks for a super magazine!